Is 2017 the Year to Move Up to Your Dream Home? If So, Do It Early!

If you are considering moving up to your dream home, it may be better to do it earlier in the year than later. The two components of your monthly mortgage payment (home prices and interest rates) are both projected to increase as the year moves forward, and interest rates may increase rather dramatically. Here are some predictions on where rates will be by the end of the year:

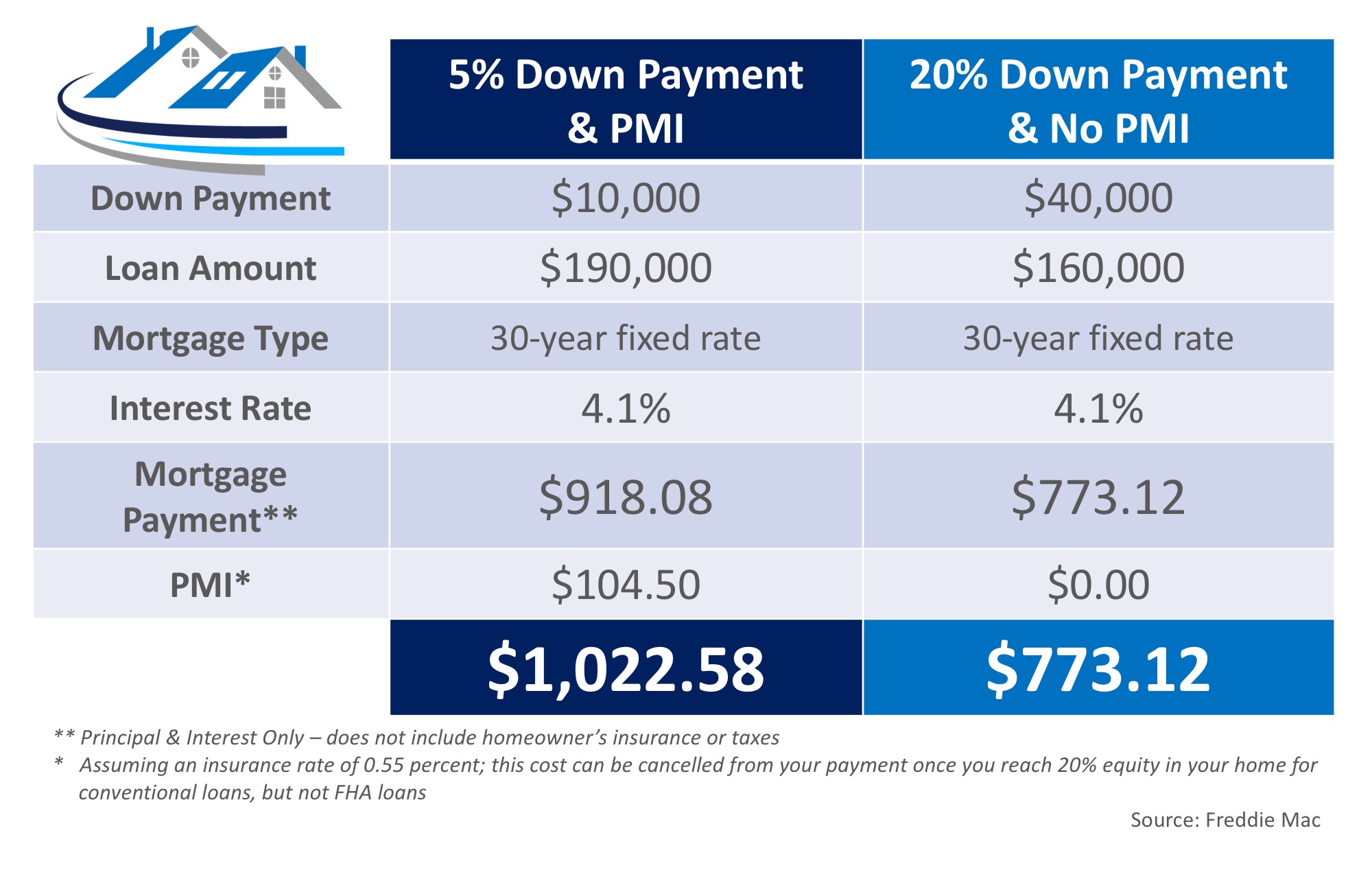

Freddie Mac

“While full employment and rising inflation are signs of a strong economy, they also have the potential to push mortgage rates and house prices up. The higher rates and higher prices create significant affordability concerns, which may continue to characterize the housing market for the rest of 2017.”

Lynn Fisher, Vice President of Research & Economics for the Mortgage Bankers Association

“By the time we get to the fourth quarter of this year, we will still be under 5 percent – we are thinking 4.7 percent…Something north of 5 percent by the time we get to 2018, and by the time we get to 2019, we show fourth-quarter rates hitting 5.5 percent.”

Mark Fleming, First American’s Chief Economist

“Despite some regional disparities, title agents and real estate professionals do not expect increasing mortgage rates to have a significant impact on the housing market this spring. Continued good economic news, increasing Millennial demand and confidence that buyers will remain in the market even if rates exceed 5 percent bode well for 2017 real estate.”

Len Kiefer, Deputy Chief Economist for Freddie Mac

“We will probably see rates higher at the end of year, around 4.5%.”

Bottom Line

If you are feeling good about your family’s economic future and are considering making a move to your dream home, doing it sooner rather than later makes the most sense.

![Do You Know the Cost of Waiting? [INFOGRAPHIC] | Simplifying The Market](https://www.truvalor.com/wp-content/uploads/2017/05/20170505-Share-STM.jpg)

![Do You Know the Cost of Waiting? [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/05/04121725/20170505-Cost-of-Waiting-STM.jpg)