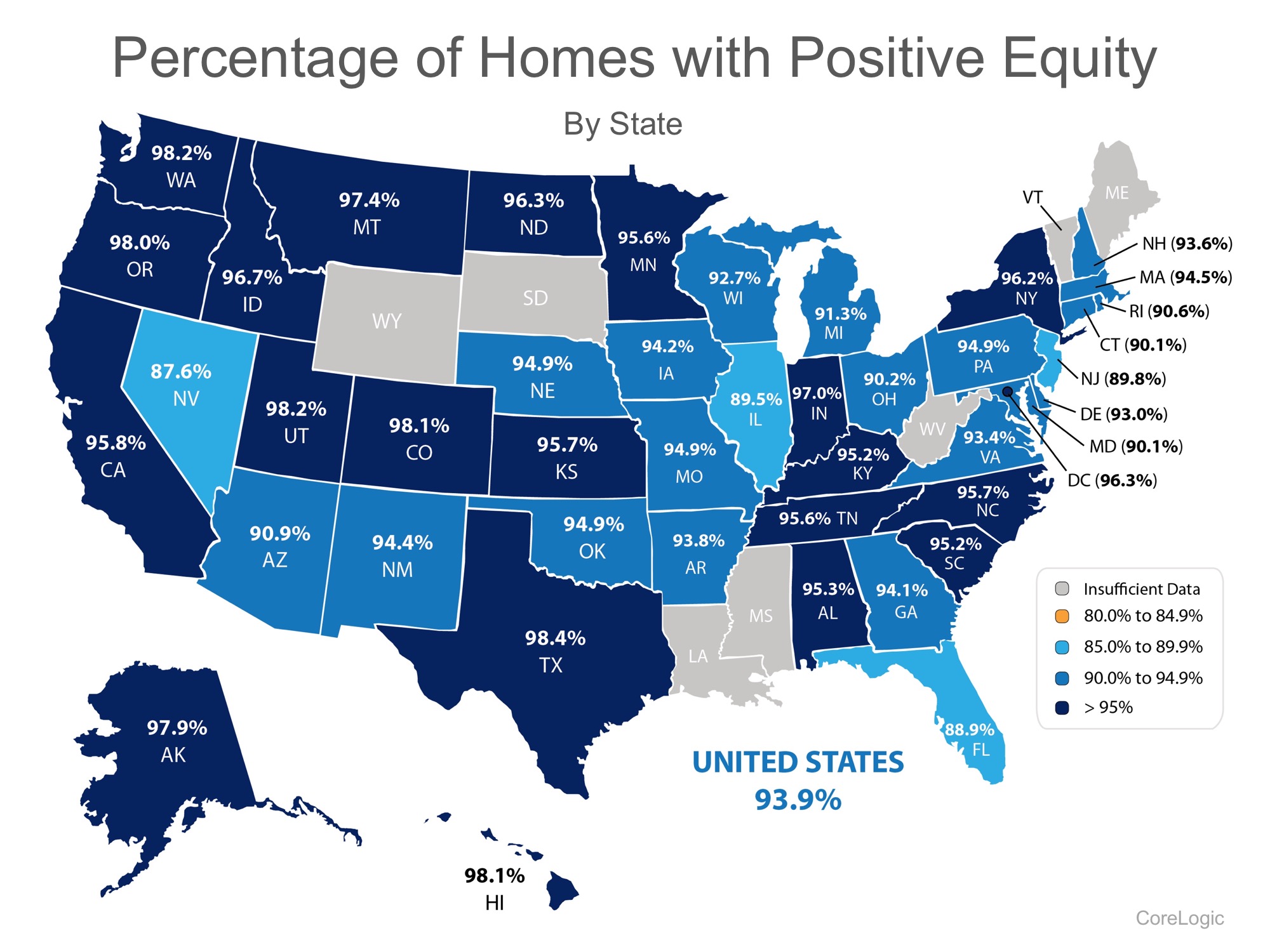

93.9% Of Homes in The US Have Positive Equity

CoreLogic’s latest Equity Report revealed that ninety-one thousand residential properties regained equity in Q1 2017. The outlook for 2017 remains positive as well, as an additional 600 thousand properties will regain equity if home prices rise another 5% this year.

The study also revealed that:

- Roughly 63% of all homeowners have seen their equity increase since Q1 2016

- The average homeowner gained about $14,000 in equity between Q1 2016 and Q1 2017

- Only 1.6% of residential properties are near-negative equity

Below is a map showing the percentage of homes with a mortgage, in each state, that have positive equity. (The states in gray have insufficient data to report.)

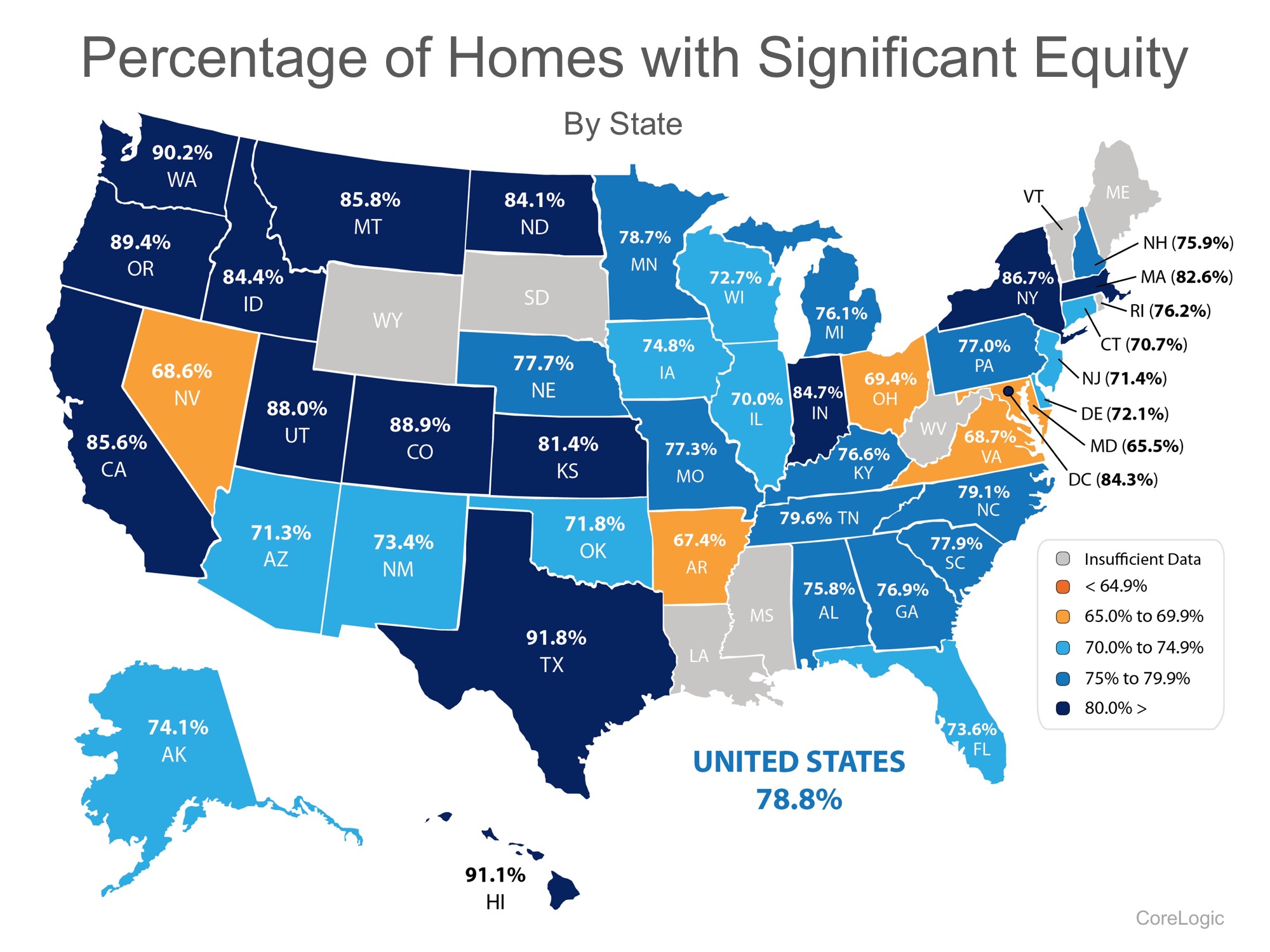

Significant Equity Is On The Rise

Frank Martell, President & CEO of CoreLogic, believes this is great news for the “long-term health of the U.S. economy.” He went on to say:

“Homeowner equity increased by $766 billion over the last year, the largest increase since Q2 2014. The rising cushion of home equity is one of the main drivers of improved mortgage performance. Since home equity is the largest source of homeowner wealth, the increase in home equity also supports consumer balance sheets, spending and the broader economy.”

Of the 93.9% of homeowners with positive equity in the US, 78.8% have significant equity (defined as more than 20%). This means that nearly three out of four homeowners with a mortgage could use the equity in their current home to purchase a new home, now.

The map below shows the percentage of homes with a mortgage, in each state, that have significant equity. (The states in gray have insufficient data to report.)

Bottom Line

If you are one of the many homeowners who are unsure of how much equity they have in their homes and are curious about their ability to move, let’s meet up to evaluate your situation.

![20 Tips for Preparing Your House for Sale [INFOGRAPHIC] | Simplifying The Market](https://www.truvalor.com/wp-content/uploads/2017/08/20170804-Share-STM.jpg)

![20 Tips for Preparing Your House for Sale [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/07/17162255/20170804-Tips-For-Selling-STM.jpg)